Founder-led is a premium. Founder-dependent is a discount. The behavioral science explains why smart founders can’t see the difference.

The deal should have closed two weeks ago. Your sales lead is good. The client is qualified. The pitch was solid. But the prospect keeps asking for “one more conversation” — specifically with you. So you block two hours on a Tuesday, get on a call, and close it. You tell yourself this is what founder leadership looks like.

What you do not tell yourself: this is the fourth time this month. And while you were on that call, three other priorities waited; one pipeline review got rescheduled, and the strategic work that would have made next quarter easier did not happen.

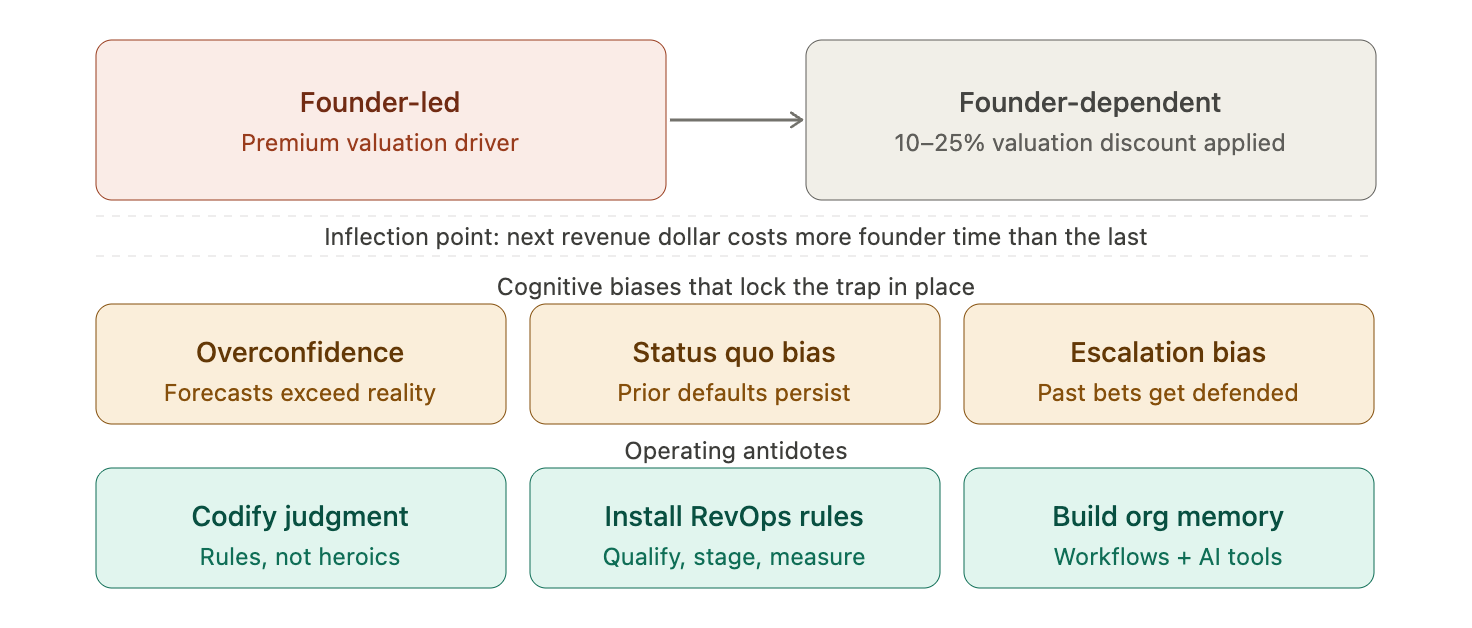

This is The Founder-Led Business Trap — the specific inflection point at which the next dollar of revenue requires more founder time than the last one. Growth is still happening. But it is no longer compounding. It is consuming. And the cognitive patterns that helped you build the business are the same ones making it nearly impossible to see.

The case for founders is real

Before making the harder argument, let’s be precise. Founder-led companies carry genuine structural advantages. Research published in the Strategic Management Journal found that founder CEOs of S&P 500 companies generate more patents — and more valuable ones — than their professional-manager counterparts (Lee, Hwang, & Chen, 2017). A Journal of Business Research study confirmed that founder CEOs can outperform agent CEOs on innovation (Kannan-Narasimhan et al., 2023). Zook (2016) documented in Harvard Business Review that founder-led companies outperform the broader market by more than three to one over time. The mechanism is straightforward: founders take longer bets, stay more committed under pressure, and act with more personal conviction than hired executives.

Founder-led, in other words, is a legitimate premium. The problem is not being founder-led. The problem is staying founder-dependent after the company has grown large enough to need systems, not just instincts.

The economic costs of the trap

Damodaran’s appraisal research documents that key-person dependency generates valuation discounts in the range of 10% to 25% or more in smaller, people-intensive firms (Damodaran, n.d.). The same business that could command a premium multiple because of founder vision commands a discount because that vision cannot be transferred. Hellauer et al. (2026) added the operational dimension in Harvard Business Review: founder CEO transitions carry a risk of failure or performance decline two to three times greater than non-founder CEO transitions. If your judgment cannot be described, repeated, or audited, you have not built a company. You have built a sophisticated job.

The commercial costs compound from there. Gartner estimates that by 2026, 75% of the highest-growth companies will adopt a RevOps model — one that unifies customer engagement and integrates people, processes, and technology to improve predictability, efficiency, and resiliency (Gartner, n.d.). When demand generation, proposals, pricing exceptions, and relationship trust all route through one person, the selling motion stays artisanal. Pipeline quality becomes volatile. Forecast accuracy degrades. Sales manager authority stays shallow. The gap between those firms and founder-dependent ones is not just operational. It is compounding.

The behavioral science underneath the trap

Here is where most strategy conversations stop — and where they should start.

The Founder-Led Business Trap persists not because founders are irrational, but because it is reinforced by entirely predictable cognitive patterns. Lee et al. (2017) found that founder CEOs use more optimistic language, issue higher earnings forecasts, and behave in ways consistent with systematically underestimating downside risk. Sharot (2011) identified optimism bias as one of the most consistent and robust findings in psychology. Combined, these two patterns explain why even experienced founders overestimate how quickly a new sales leader will ramp, how easily an artisanal offer can be standardized, or how soon the team will “pick it up” without real process design.

Status quo bias compounds the error: Samuelson and Zeckhauser (1988) showed that people disproportionately prefer existing arrangements independent of their actual merit, while Staw (1976) demonstrated that decision-makers often commit even more resources to a failing course when they are personally responsible for it. Kahneman and Tversky’s (1979) prospect theory explains the emotional mechanism underneath both: losses loom larger than equivalent gains. Transferring a key customer relationship can feel like losing status. Resetting pricing can feel more painful than the cost of continuing to discount. Changing a signature offer can feel like admitting the original design failed.

The trap is not irrational. It is deeply rational — from inside the cognitive frame the founder built over years of early success.

Here is how those dynamics interact with the business economics:

What the trap actually looks like — and what Benioff built instead

In the past year, I’ve sat across from three different founders who were living the same day.

One runs a $10 million B2B technology services firm. One runs a $22 million financial advisory practice. One runs a $27 million healthcare consulting group. Different industries, different products, different teams. The same trap.

In each case, the founder was personally involved in more than half of all active opportunities — not because they were micromanaging, but because they were the only person who could close the room. In each case, gross margins had quietly compressed as founder time became the default cost of anything complicated. Delivery escalations routed back through the founder. Pricing exceptions required a founder call. Key renewals were relationship-dependent in a way no account manager could replicate without one. The CRM, in each case, was really a contact list.

Each of these business is operationally viable — but not yet sellable. Any serious acquirer would trace the revenue back to one person’s calendar and reprice accordingly.

This is The Founder-Led Business Trap in its most common form. Not a governance collapse. Not a culture crisis. A quiet arithmetic problem: the company grows until it bumps against the ceiling of one person’s available hours, and then it stops. Revenue becomes lumpy. Pipeline visibility degrades. And the founder, who has built something genuinely valuable, cannot extract full value from it — because the value and the founder are still the same thing.

None of these three founders were weak operators. All three had built something real. The trap had nothing to do with talent and everything to do with architecture — specifically, the absence of systems designed to carry founder judgment without requiring founder presence.

Marc Benioff solved this problem before it had a chance to become one.

Salesforce’s V2MOM — Vision, Values, Methods, Obstacles, Measures — started as a four-person alignment document in 1999 and became the operating system that now cascades across one of the most valuable enterprise software companies in the world. Benioff has described V2MOM as simultaneously the company’s business plan and its cultural spine — a structure that makes priorities, tradeoffs, and decision logic visible to everyone, at every level, without requiring Benioff in the room (Benioff, 2024). The FY2026 results are the proof of concept: $41.5 billion in revenue, a 20.1% GAAP operating margin, and $15.0 billion in operating cash flow (Salesforce, 2026).

That is what founder vision looks like when it is systematically translated into structure rather than left as personal intuition.

The lesson is not that every founder needs V2MOM. It is that Benioff made a specific architectural choice early: his judgment would become a system, not a dependency. He converted founder instinct into shared language, shared priorities, and shared accountability that could scale without him at the center of every decision. The three founders I described above had not yet made that choice — not because they lacked ambition, but because The Founder-Led Business Trap is most comfortable when the company is still growing and the founder is still winning. The urgency is hard to feel when the pipeline is moving and the clients are calling.

The behavioral science explains precisely why that window closes faster than most founders expect.

The move you need to make

The strategic answer to The Founder-Led Business Trap is not to become less of a founder. It is to make your founder judgment transferable.

McKinsey (2022) identifies the operating rule that matters most at scale: gather perspectives broadly, but be unambiguous about who has the final say. Amazon’s decision architecture — distinguish reversible from irreversible, act on 70% of desired information, disagree and commit — gives that principle its operational teeth (Bezos, 2018). For marketing and revenue leaders, the parallel work is converting founder credibility into transferable market proof: role-specific case studies, ROI evidence, and customer language that a sales champion can carry internally without requiring a founder-level relationship (Smith, 2026b). For operations and finance, it means converting tribal knowledge into institutional memory — standardized workflows, AI-assisted reporting, and the KPI layer that tells you whether the business is actually de-risking itself: founder hours in selling and delivery, pipeline value independent of founder involvement, close rate, gross margin, and recurring revenue percentage (Barros et al., 2015; Bezos, 2018).

The diagnostic you cannot avoid

If you took a 60-day leave of absence tomorrow, what would break in your pipeline? What would your team not know how to price? Which customer relationships would stall? How many proposals would not get written?

Those answers tell you exactly how much of your enterprise value is sitting in one person’s calendar right now. And they tell you precisely how deep into The Founder-Led Business Trap your company currently sits.

Founder-led is still a premium. The market rewards founder vision, conviction, and speed. But the same market applies a significant discount when that vision cannot outlast a single person’s attention span.

The most valuable thing a founder can build this year is the system that makes them less necessary to it.

About Rich Smith: Rich Smith is an executive advisor, behavioral marketing strategist, investor, CMO, and host of the Revenue Science Podcast, known for helping leaders understand not only what growth strategies work—but why. With more than thirty years of experience leading growth across financial services, healthcare, technology, and consumer brands, Rich has guided companies through crises, rebuilt brands from the ground up, and helped position organizations for nine-figure exits. Connect at RichMSmith.com, on LinkedIn, and on The Revenue Science Podcast.

References

Barros, V. F. A., Ramos, I., & Perez, G. (2015). Information systems and organizational memory: A literature review. Journal of Information Systems and Technology Management, 12(1), 45–64.

Benioff, M. (2024, December 11). Create strategic company alignment with a V2MOM. Salesforce. https://www.salesforce.com/blog/how-to-create-alignment-within-your-company/

Bezos, J. (2018, March 21). Jeff Bezos’ 2016 letter to Amazon shareholders. About Amazon. https://www.aboutamazon.com/news/company-news/2016-letter-to-shareholders

Damodaran, A. (n.d.). Key person [Presentation]. Stern School of Business, New York University. https://pages.stern.nyu.edu/~adamodar/pdfiles/blog/KeyPerson.pdf

Gartner. (n.d.). Revenue operations: The what, best practices & RevOps guide. https://www.gartner.com/en/sales/topics/revenue-operations

Hellauer, S., Kos, S., Vermoort, J., Sadarangani Werner, S., & Wright, B. (2026, January–February). Leading after the founder. Harvard Business Review.

Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263–291.

Kannan-Narasimhan, R. P., Wang, R., & Zhu, P. (2023). Founder versus agent CEOs: Effects of founder status and power on firm innovation and cost of capital. Journal of Business Research, 166, 114180.

Lee, J. M., Hwang, B.-H., & Chen, H. (2017). Are founder CEOs more overconfident than professional CEOs? Evidence from S&P 1500 companies. Strategic Management Journal, 38(3), 751–769.

McKinsey & Company. (2022, November 9). Scaling up: How founder CEOs and teams can go beyond aspiration to ascent.

Salesforce. (2026, February 25). Salesforce delivers record fourth quarter fiscal 2026 results.

Samuelson, W., & Zeckhauser, R. (1988). Status quo bias in decision making. Journal of Risk and Uncertainty, 1, 7–59.

Sharot, T. (2011). The optimism bias. Current Biology, 21(23), R941–R945.

Smith, R. (2026a, April 15). Social proof at scale: Engineering credibility for mid-market growth. Rich Smith’s Blog. https://richmsmith.com/

Smith, R. (2026b, May 12). Growth is not a channel problem. It’s a behavior design problem — here’s the system. Rich Smith’s Blog. https://richmsmith.com/growth-is-not-a-channel-problem-its-a-behavior-design-problem-heres-the-system/

Staw, B. M. (1976). Knee-deep in the big muddy: A study of escalating commitment to a chosen course of action. Organizational Behavior and Human Performance, 16(1), 27–44.

Tversky, A., & Kahneman, D. (1974). Judgment under uncertainty: Heuristics and biases. Science, 185(4157), 1124–1131.

Zook, C. (2016, March 24). Founder-led companies outperform the rest — here’s why. Harvard Business Review. https://hbr.org/2016/03/founder-led-companies-outperform-the-rest-heres-why